Accepting Payment Cards

Overview

Wake Forest accepts credit and debit card payments (MasterCard, Visa, Discover and American Express) for non-student account related transactions. Typically, these payments are for conferences, workshops, services, educational materials, etc.

Wake Forest University is required by the credit card associations to be compliant with the Payment Card Industry Data Security Standards (PCIDSS), and is committed to providing a secure environment for our customers to protect against both loss and fraud. University merchants comply with these standards by securely processing, storing, transmitting and disposing of cardholder data.

Due to the complexities and security requirements associated with the acceptance of payment cards, please contact Finance well in advance of needing to accept card payments.

For questions relating to payment card acceptance, merchant accounts, or accounting, contact in Finance .

For questions relating to the University Payment Card Compliance Committee or equipment and software, contact Information Security.

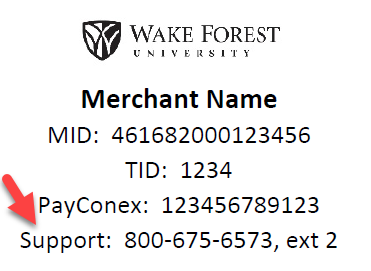

For payment card terminal support, contact the support number located on the label on your machine. The label will look like this:

If there is concern that a card or card sales is suspicious, contact American Express at 800.528.2121 or all the other card brands at 800.291.4840. Be sure to have your Merchant ID ready and reference the term ‘Code 10’.

Becoming a Merchant

In order to become a campus merchant, departments, organizations and affiliates need to familiarize themselves with the Payment Card Acceptance Administrative Policy and related Procedure. These documents specify initial and ongoing roles, responsibilities and expectations. To request to become a campus merchant, submit your request via Workday. Choose the ‘Finance Payment Card New Merchant Request’ request type. Be sure to answer all questions and submit all available documentation.

FAQ

Note: The files associated with the processes to Accept Payment Cards are accessible to WFU users via Google Drive. If you are not signed in to Google, you will be asked to sign in with your Wake Forest username and password prior to accessing related files.

Truist Merchant Connection is the reporting service from Truist, which is the University’s standard payment card processor. Authorization logs are real-time. Standard financial reports for the prior day are available each day at 9am. Only one merchant account can be accessed at a time.

- To get an account, contact Renee Wilkins in Finance.

- If you have forgotten your username or password or locked your account, contact the Truist Support Center at 877.672.4228, option 0. They will only assist someone who is listed on the merchant account as an authorized user.

- To learn more about running reports, click on the ‘Help’ menu item in the top right of the screen or click here. Then click on ‘Run a Report’ for information about what reports are available and how to run them.

Commerce Manager is the standard payment gateway for e-commerce transactions throughout campus. Several resources are available to learn about using the system:

- Running Commerce Manager Reports for Depositing Funds with the Cashier (PDF): Follow these instructions to execute the required reporting to submit the payment card type breakdown to the cashier in Finance.

- Commerce Manager Administrative Guide: A comprehensive guide is available through the NBS HelpHub and can be used by Commerce Manager Customer Service Representatives (CSR) who manually key in card transactions via a Bluefin P2PE device and Reporters to extract summary and detail transaction information. To gain access to the HelpHub, email p to have a username and password assigned.

The Commerce Manager Administrative Guide should also be used to guide the integration between departmental, event or conference websites and the Commerce Manager payment pages. Supplemental interfacing information is also available from Information Security.

IMPORTANT! Departments are responsible for obtaining all resources in order to build their own departmental, event or conference websites and integrating them with Commerce Manager.

Finance has cellular / wireless payment (credit and debit) card devices which can be used by any Wake Forest University department, organization or affiliate holding an authorized University event. To get started, read the rental request instructions.

Prior to submitting a request, it is important that you familiarize yourself with the Payment Card Acceptance Merchant Procedures, especially if this is going to be the first time you are using one of our standby accounts.

IMPORTANT! In the event that the device is stolen or there is a suspicion of a loss of data due to a security breach (e.g. suspected virus infection or unusual activity on the terminal), immediately report the concern to Information Security. Finance and Information Security will assess the situation and invoke the necessary incident response plan.

Departments are responsible for making all deposits relating to payment cards. Regardless of the way payment cards are accepted (Commerce Manager, physical terminals, etc.), a settlement report should be printed showing the breakdown by card type (e.g. Master Card, Visa, Discover, or American Express). Attach this settlement report to the deposit form, which should also have the amounts broken down by card type. For more information, please review to the following guides:

Tools

Note: The files associated with the processes to Accept Payment Cards are accessible to WFU users via Google Drive. If you are not signed in to Google, you will be asked to sign in with your Wake Forest username and password prior to accessing related files.

- Device User Guides

- Software User Guides

- Merchant Services Glossary

Forms

- Rental Request Form (be sure to read the instructions first)

- PCI Security and Confidentiality Agreement (Google Document)

- Wake Forest University Payment Card Terminal Inspection Log (PDF)